What Credit Score Do You Need to Buy a Home?

Your credit score is one of the most important factors in determining whether you’ll qualify for a mortgage and what interest rate you’ll receive. Understanding credit score requirements for different loan types can help you prepare financially and potentially save thousands of dollars over the life of your loan.

Credit Score Requirements by Loan Type

Different mortgage programs have varying credit score minimums, making homeownership accessible to buyers across different credit profiles.

FHA Loans: Most Accessible Option

Federal Housing Administration loans offer the most lenient credit requirements, making them popular with first-time homebuyers.

Minimum Credit Score: 580 for 3.5% down payment. Alternative Option: 500-579 credit score with 10% down payment

Most FHA-approved lenders, however, set their own minimum at 620 to minimize risk. Even with a 580 score, you’ll need compensating factors like stable employment, a low debt-to-income ratio, or significant cash reserves to strengthen your application.

FHA loans require mortgage insurance for the life of the loan if you put down less than 10%, which adds to your monthly payment but makes homeownership possible with less-than-perfect credit.

Conventional Loans: Standard Requirements

Important Update: As of November 16, 2025, Fannie Mae and Freddie Mac removed minimum credit score requirements from their conventional loan guidelines. However, individual lenders still maintain their own standards.

Typical Lender Minimum: 620 credit score, Optimal Range: 740+ for best rates and terms

While 620 is the general threshold, borrowers with scores in the 740+ range receive significantly better interest rates and more favorable terms. A conventional loan becomes particularly attractive if you can make a 20% down payment, eliminating private mortgage insurance entirely.

For borrowers with multiple applicants, Fannie Mae now averages the median scores of all borrowers rather than using the lowest score, making it easier for couples with different credit profiles to qualify.

VA Loans: Flexible for Veterans

The Department of Veterans Affairs doesn’t set a minimum credit score requirement for VA loans, but lenders establish their own standards.

Typical Lender Minimum: 620 credit score. Some Lenders Accept: 580 with strong compensating factors

VA loans offer exceptional benefits for military service members and veterans, including no down payment requirement and no private mortgage insurance. Even with a lower credit score, veterans may qualify through manual underwriting if they demonstrate high residual income and a stable employment history.

USDA Loans: Rural Property Financing

USDA loans, designed for rural and suburban homebuyers, also rely on lender-specific requirements rather than a government-mandated minimum.

Typical Lender Minimum: 640 credit score, Automated Underwriting Threshold: 640 for USDA’s Guaranteed Underwriting System

USDA loans require no down payment and offer competitive rates, but they’re limited to properties in USDA-eligible rural areas and come with income limits based on household size and location.

How Credit Scores Impact Your Mortgage Rate

Your credit score doesn’t just determine whether you qualify—it dramatically affects your interest rate and total loan cost.

Real-World Rate Differences

On a $300,000 mortgage with a 30-year term, here’s how credit scores typically impact rates:

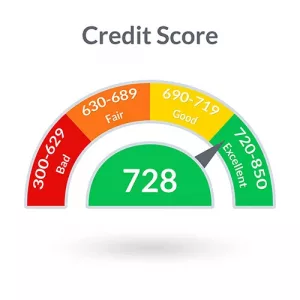

Excellent Credit (760-850): ~6.5% interest rate

- Monthly payment: $1,896

- Total interest paid: $382,560

Good Credit (700-759): ~6.8% interest rate

- Monthly payment: $1,957

- Total interest paid: $404,520

Fair Credit (640-699): ~7.3% interest rate

- Monthly payment: $2,046

- Total interest paid: $436,560

Poor Credit (580-639): ~8.0% interest rate (if approved)

- Monthly payment: $2,201

- Total interest paid: $492,360

The difference between excellent and fair credit on this loan amounts to $54,000 over 30 years—a high cost of lower credit scores.

What Makes Up Your Credit Score?

Understanding the components of your credit score helps you focus improvement efforts where they matter most.

Payment History (35%): Your track record of on-time payments is the single most important factor. Even one 30-day late payment can drop your score by 60-110 points.

Credit Utilization (30%): This is the ratio of your credit card balances to credit limits. Keep utilization below 30% per card, ideally below 10%, for optimal scores.

Length of Credit History (15%): The age of your oldest account, newest account, and average age of all accounts. Closing old accounts can hurt your score.

Credit Mix (10%): Having different types of credit—credit cards, auto loans, mortgages—demonstrates you can manage various obligations.

New Credit Inquiries (10%): Each hard inquiry from a credit application can temporarily lower your score by a few points. Multiple mortgage inquiries within 45 days count as one inquiry.

Improving Your Credit Score Before Applying

If your credit score falls below your target range, strategic actions can boost your score within months.

Quick Wins (30-90 Days)

Pay Down Credit Card Balances: Reducing utilization from 50% to 10% can increase your score by 50+ points within one billing cycle.

Dispute Credit Report Errors: Check your reports from all three bureaus at AnnualCreditReport.com and dispute any inaccuracies. Errors corrected within 30-45 days can immediately improve your score.

Become an Authorized User: If a family member adds you to their established credit card with excellent payment history, it can boost your score quickly.

Request Higher Credit Limits: If you have good payment history, requesting credit limit increases lowers your utilization ratio without changing your spending.

Medium-Term Strategies (3-6 Months)

Set Up Payment Reminders: Payment history is crucial. Use autopay or calendar alerts to ensure every bill is paid on time.

Pay Collections or Charge-Offs: While paying old debts doesn’t remove them from your report, it shows responsibility and may be required by lenders.

Use Experian Boost: This free service adds utility and phone bill payments to your credit file, potentially boosting your score.

Reduce Overall Debt: Focus on high-interest debt first, while making minimum payments on everything else.

What to Avoid

Don’t Close Old Credit Cards: This reduces your available credit and can increase utilization. Keep old cards active with small, occasional purchases.

Don’t Apply for New Credit: Each application creates a hard inquiry. Wait until after your mortgage closes to open new accounts.

Don’t Make Large Purchases: Financing furniture or a car before your mortgage closes can increase your debt-to-income ratio and jeopardize approval.

Don’t Co-Sign Loans: Taking on someone else’s debt obligation affects your qualification, even if you’re not making the payments.

Special Considerations for Arizona Homebuyers

In Tucson and across Arizona, the median home price ranges from $315,000 to $375,000 depending on location. Here’s how credit scores translate to qualification in the local market:

For a $350,000 home with 5% down:

- Excellent credit (740+): ~6.5% rate, $2,192 monthly payment

- Good credit (680-739): ~7.0% rate, $2,213 monthly payment

- Fair credit (620-679): ~7.5% rate, $2,330 monthly payment

That 1% rate difference costs $138 per month or $49,680 over the loan’s life—a strong incentive to improve your score before applying. Calculate your potential mortgage payment based on your credit profile.

When to Wait vs. When to Buy Now

Consider waiting if:

- Your score is below 580, and you need an FHA loan

- You have recent late payments in the past 12 months

- You’re actively disputing errors that could raise your score

- You can realistically improve your score by 40+ points in 3-6 months

Move forward now if:

- You meet the minimum requirements for your target loan type

- You have a stable income and a low debt-to-income ratio

- Home prices or interest rates are trending upward in your market

- You have strong compensating factors despite a lower score

- Waiting would cost you more in rising prices than you’d save with a better rate

Working With Lenders on Credit Issues

Even if your credit score is below ideal, experienced loan officers can often find solutions.

Manual Underwriting: For borrowers slightly below minimum scores, manual underwriting examines your full financial picture rather than relying solely on automated systems. Strong employment history, significant savings, or low housing expense ratios can overcome lower scores.

Non-Traditional Credit: If you have limited credit history, some programs accept alternative documentation, such as rental payment history, utility bills, or insurance payments, to demonstrate creditworthiness.

Rapid Rescore: If you’ve recently paid down debt or corrected errors, your lender can request a rapid rescore to update your credit report within days, rather than waiting 30-45 days for a normal reporting cycle.

The Bottom Line

While minimum credit scores vary by loan type—from 500 for FHA with 10% down to 620 for conventional loans—your actual credit score significantly impacts your mortgage rate and total cost. Every 20-40 point improvement in your score can lower your rate and save thousands in interest.

The good news is that credit scores can be improved. Strategic focus on payment history, credit utilization, and error correction can boost your score within months, putting you in a stronger position to qualify for better loan terms.

Ready to Explore Your Options?

Your credit score is just one part of your mortgage application. Our experienced loan officers at Altitude Home Loans understand that every borrower’s situation is unique. We work with borrowers across all credit profiles, helping you understand your options and find the best loan program for your circumstances.

Contact us today for a free consultation. We’ll review your credit profile, explain which loan programs you qualify for, and create a strategy to help you achieve homeownership—whether that means moving forward now or taking steps to improve your credit first.

Proof of Income

Proof of Income You do not have to own a business to be self-employed. A mortgage lender considers the following people also to be

You do not have to own a business to be self-employed. A mortgage lender considers the following people also to be

Assets that have a cash value or can be converted to cash are called liquid assets. Lenders would want to verify that you have the means to pay the payments, insurance, taxes, and interest on your mortgage. The capability to pay for these is determined by the liquid assets, including bank account, savings account, checking account, stock option, etc. Experts suggest having six months of current income in liquid assets or cash to tide you over in times of financial emergency. This ensures that you can continue paying the mortgage payments even if you have no source of income.

Assets that have a cash value or can be converted to cash are called liquid assets. Lenders would want to verify that you have the means to pay the payments, insurance, taxes, and interest on your mortgage. The capability to pay for these is determined by the liquid assets, including bank account, savings account, checking account, stock option, etc. Experts suggest having six months of current income in liquid assets or cash to tide you over in times of financial emergency. This ensures that you can continue paying the mortgage payments even if you have no source of income. Title Search and Insurance

Title Search and Insurance

Acquiring a mortgage can be a stressful and pretty complicated process, not to mention competitive. To make everything easier, here are a few

Acquiring a mortgage can be a stressful and pretty complicated process, not to mention competitive. To make everything easier, here are a few  A mortgage is a loan that a borrower uses to buy real estate like a home or other property. The property itself acts as collateral for the loan. The loan is then repaid over a period of time in a series of monthly mortgage payments.

A mortgage is a loan that a borrower uses to buy real estate like a home or other property. The property itself acts as collateral for the loan. The loan is then repaid over a period of time in a series of monthly mortgage payments. There’s a lot more you need to consider than the mortgage rate when getting a home loan. The following questions can help you with the important questions you may want to ask your lender.

There’s a lot more you need to consider than the mortgage rate when getting a home loan. The following questions can help you with the important questions you may want to ask your lender. Even though it looks like a lender can ask any

Even though it looks like a lender can ask any